How markets have performed (to end September 2018)

The summer months passed largely without incident in financial markets. The divergence between the US and the rest of the world that began in June continued unchecked through July and August. Emerging markets bore the brunt of the weakness as worsening news flow on the situation in Turkey and Argentina soured investor sentiment and the ongoing trade tensions between the US and China placed further pressure on Asian financial markets. As a result, both EM equity and debt assets have suffered significant markdowns. The US stock market continued its dominance in performance terms, outperforming all other equity regions – led higher by a relatively narrow cohort of well-known growth stocks. In the fixed income markets, yields have risen modestly but credit spreads in corporate debt have been broadly stable. Oil has risen consistently over the summer, with Brent Crude trading near a 4 year high of $80/barrel. Gold has steadily lost ground in the face of the march higher in risk assets, trading down to c.$1200/oz at the time of writing. For UK investors, Sterling saw a sharp move higher in early September as rumours of concessions from the EU in the Brexit negotiations led to expectations for a deal resolution – the Austrian meeting of the EU in mid-September dented this optimism and some of these gains reversed.

What are we thinking

From our recent asset allocation meeting, and conversations with a range of investors in the markets, we agree with Byron Wien of Blackstone’s assessment of market sentiment in his summer letter – investors are generally ‘talking worried but being complacent’.

In the short term strong economic data, predominantly from the US, and corporate earnings boosted significantly by the tax reform earlier this year, have allowed equity markets in the US to move higher. Positive, but muted, growth in GDP and earnings in other regions has translated into weaker returns.

It is easy to identify many potential risks on the horizon – building inflation pressure from tight labour markets, asset valuations, geopolitical concerns and the unknown path to the ultimate resolution of the trade protectionism skirmishes, to name a few – from which one could draw a very negative outlook.

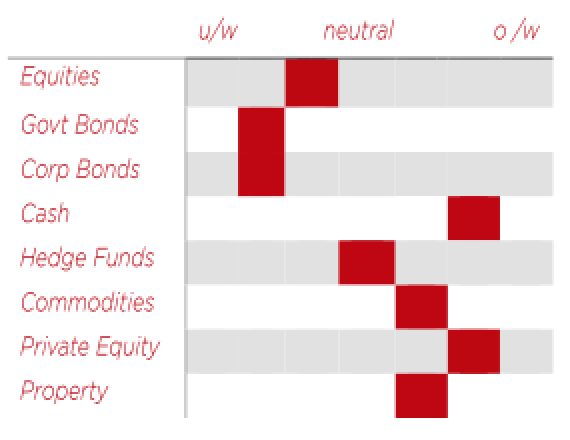

We have not made any investment strategy changes of note over the summer months. We remain modestly defensive, having taken some profits from a long-standing equity overweight as markets rose during the year. Within portfolios we hold a barbell exposure, with a bias towards cheaper (but more volatile) value style equity strategies balanced with an overweight exposure to cash and gold as a defensive allocation.

Insights from some of our managers

A common theme amongst value managers we have met recently is a large portfolio exposure to financials, and banks especially. Having been at the epicenter of the prior crisis, these companies have seen huge restructuring in the prior decade with increased regulatory scrutiny, balance sheet repair and extensive fines for poor conduct. Investor sentiment remains in the doldrums but we have heard several convincing cases that the multiple headwinds these companies are facing are dissipating, and in a world of rising interest rates their profitability could stand to surprise investors who have dismissed the sector.

Other news

As demand for sustainable and impact investing grows, we are finding that our bespoke approach fits well with families and endowments who want to align their portfolios with their values. Furthermore, our quantitative research suggests that global equity funds that are managed with an ESG (Environmental, Social and Governance) focus do not underperform “traditional” global equity funds. There is, however, a large dispersion of returns between ESG managers.