How markets have performed (to end September 2020)

The market recovery of the second quarter continued over the summer months. However, a notable feature of the past quarter has been the imbalanced recovery from the deep COVID-19 induced recession, with plentiful liquidity provided by politicians and policymakers quelling the worst fears of the financial markets, but leading to a huge dispersion in performance.

The US equity market, and a handful of its growth-oriented technology and communications companies, dominated the headlines and were the core contributors to market returns. The fortunes of these better performing stocks dimmed in September as investors took pause amid fears of a second wave of COVID 19 and the pending US election. By contrast, the UK market has not experienced the same level of recovery, owing to the structure of the UK stock market (heavily exposed to financials, energy, and mining) and renewed caution over the path of the Brexit negotiations.

Bond yields traded within a reasonably tight range over the summer months, with credit spreads grinding tighter as economic conditions improved and investor sentiment remained buoyant. Meanwhile, Gold remains one of the stand-out performers for the year to date, briefly breaching the $2000/oz mark in the summer months.

What we are thinking

As the US presidential election approaches, the final quarter of 2020 may provide further bouts of volatility as investors weigh up the implications of both candidates. President Trump’s COVID diagnosis and the unpredictable negotiations for a second stimulus package for the US economy throw in more uncertainty. There is a reasonable chance of a prolonged and contentious election result reminiscent of the 2000 ‘hanging chads’ decided by the US courts which would be a dangerous environment for a still fragile economy and market. What seems to be a bipartisan position is a wariness towards China, and therefore we believe trade tensions are likely to remain heightened regardless of the victor.

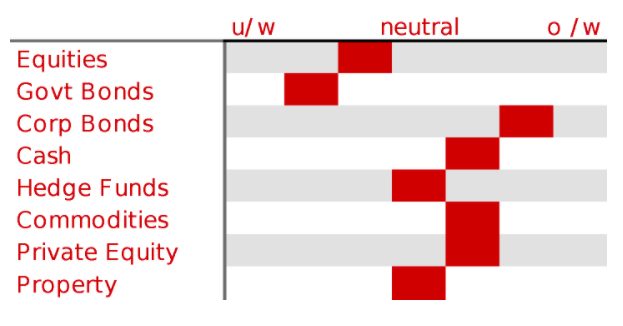

During the summer we took advantage of periods of weakness to increase equity exposure selectively, but overall, we retain a slight underweight equity position given the elevated valuation levels of the aggregate market. Broadly, portfolios are allocated to resilient companies which can survive the acute stresses of 2020 and to be in a position to benefit beyond this, but which are trading at reasonable valuations.

Within bonds we retain a significant exposure to Investment Grade and High Yield bonds where we believe the yields on offer deliver a margin of safety relative to expected defaults. We will broaden this allocation with an investment in a senior secured bond fund in the coming quarter, as well as an initial allocation to Chinese government bonds, denominated in RMB. We believe that the market offers an attractive yield, solid credit fundamentals and a sustained capital tailwind as the longer-term program of broadening and deepening the Chinese financial markets through internationalisation continues.

We retain a position in gold bullion as a diversifying asset and portfolio protection.

Insights from some of our managers

We have recently met a number of quality/growth focused UK managers which, given their style tilt and the prevailing market dynamics, have delivered strong relative returns. What is interesting, however, is that for some of the best performing managers, these excess returns have been derived from their flexibility to invest in non-UK stocks and in one case the manager’s largest performance contributor was Microsoft! This highlights the challenges faced by UK equity managers to find opportunities in a market that is struggling to recover from the deep recession and structurally biased towards energy, resources and the financial sectors.

Other news

Zoom Video Communications is undoubtedly one of the biggest winners of 2020 as enforced lockdowns worldwide saw a need for families, friends and working colleagues to find a simple, easy-to-use video conferencing interface to maintain contact. Zoom fulfilled this need and has seen its share price rise from under $70 to $555 this year, resulting in the company being worth more than former tech powerhouse IBM, at over $150 billion.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.