How markets have performed (to end October)

Emerging market equities have been the strongest performers this year, led by Brazil and Russia. Corporate bonds have continued to rally as spreads tightened and government rates have plunged to record lows. In currencies, the Yen has strengthened and sterling has weakened. Iron ore, Gold and Oil have all had very strong years so far.

What we are thinking

The early conclusion of our recent ‘House View’ Investment discussion was that we are at a turning point which will impact the global economy, growth, inflation, interest rates and trade. The unexpected outcomes of the UK Referendum and US Presidential elections we believe are evidence of this turning point, and their mandates will have longstanding and significant impacts on the course of our prosperity. We expect that a combination of protectionism, fiscal policy stimulus and re-distributive wealth measures will have a short term positive impact on economic growth, eroded thereafter by the headwinds of demographics, productivity and debt burdens. We feel that inflationary pressures will rise, and be persistent, and therefore we are re-evaluating our portfolio positioning to reflect this change of view. We believe domestic US Smaller companies will be strong beneficiaries of these trends.

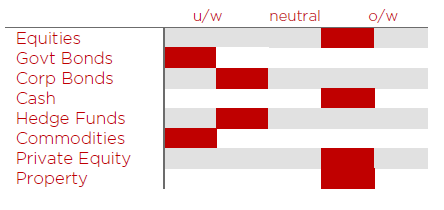

Our latest view on asset allocation positioning

Insights from some of our managers

A global growth manager reported a significant rotation in their investment strategy. They are replacing the sectors recently synonymous with growth investing (Biotech, Technology and Internet related companies), fearing that their lofty valuations will not be supported by the corporate earnings potential. Instead they have turned their attention to companies who have latent growth potential in their businesses which can be unlocked through internal change, rather than relying on external factors.

One of our Asian equity managers has applied a similar change to their strategy, turning their back on quality growth companies in the region (deemed to be fairly priced) and buying out of favour cyclical businesses which they believe offer an attractive asymmetry and potential for greater profits given their cheap valuations.

Other news

The latest evidence of the hunt for yield and duration came on the 24th October when Austria sold 2 billion euros of bonds maturing in 70 years’ time and yielding 1.5%. This sale follows this year’s 100 year bond offerings from Belgium and Ireland, as well as 50 year deals from France, Italy and Spain. The duration risk keeps piling up: the amount of government debt due in 10 years or more has grown by $733 billion this year. The effective duration on Bank of America’s global bond index has increased to 8.23, from 5 in 1997. This means that a one percentage point increase in interest rates could result in about $2.1 trillion in losses for global bond investors.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our clients’ expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multifamily offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and

adherence to putting clients’ interests first.