How markets have performed (to end April 2017)

April was far from smooth sailing. It was a muted month initially where markets were weighed upon by the disappointment of the US health care vote and rising geopolitical tensions in the Korean peninsula. However, a market friendly French election first round result coupled with a strong start to earnings season on both sides of the pond helped risk assets stage a decent rally, with Europe leading the way. Fixed income markets were well supported, credit marginally outperformed the government markets. Returns for sterling based portfolios were somewhat suppressed as a resurgent pound dimmed the returns from international assets.

What we are thinking

We do not believe that the last two months mark the end of the reflation trade, and we retain conviction in our House View strategy for client portfolios. Many business confidence indicators point to an optimistic mood among business leaders, confidence is also high among consumers and investors. The buoyancy of these ‘soft economic’ indicators are divergent from the ‘hard data’ of GDP published thus far, and we subscribe to the view that the weakness of the official data is a transient factor which will improve as the year progresses. We are also encouraged by the positive developments in the expectations of corporate earnings.

As one political risk has diminished (French Presidential elections) a new one has appeared on the radar (UK General Election). We are also increasingly concerned about the risk from Italy. Elections there are on the horizon with electorate sentiment deteriorating and populists gaining support. In the UK, the announcement of a General Election was unexpected, but not a complete shock given the data of the opinion polls. The markets have reacted positively to the news, the expectation being for a landslide result in favour of the Conservatives. Sterling has been a primary beneficiary, rising close to $1.30 in the weeks following the election announcement. We fear this optimism is likely to be short-lived. The key to our pessimism is the UK current account deficit, which viewed relative to GDP is more negative than ever before, even 1976 when the UK applied to the IMF for a bailout.

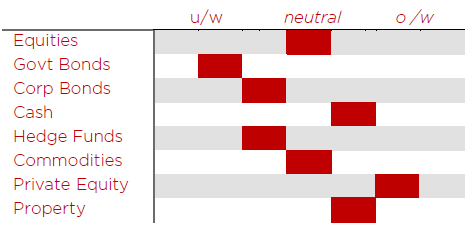

We made no changes to our investment strategy during the month, however, we are considering increasing exposure to Asia, where certain market valuations look attractive.

Our latest view on asset allocation positioning

Insights from some of our managers

A compelling case was put forth by a specialist debt manager lending directly to the small business sector of the German economy (the Mittelstand). They report a huge retrenchment from the market by traditional bank lenders, their ability to lend curbed by the need to repair their balance sheets and stringent banking regulation. A large swathe of established businesses are therefore potentially starved of the debt financing required to operate and grow. An imbalance of demand and supply is typically a fertile investment opportunity, and we are allocating research resource to investigate the opportunity further.

Other news

The Apple share price closed on 9th May with a market cap of over $800bn ($803bn to be precise), the first US company to reach such levels. This time last year it was $508bn. At its current size it is equivalent to the sum of the market caps of the smallest 103 companies in the S&P500.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.