How markets have performed (to end February 2017)

A mixed, but positive month overall for assets. There was a slight divergence of performance between assets sensitive to President Trump’s policies and European assets, which were held back by trepidation of the upcoming electoral cycle. EM assets continued to perform strongly, however investor nervousness was highlighted by strong returns during the month for Gold and Silver, a sign of a desire by investors to have tail risk or inflation hedges in place.

What we are thinking

One of the key topics of our 2017 House View investment strategy is our expectation for monetary policy and the role of the central banks. We believe that the stimulative impact of monetary policy is almost exhausted, and as politicians and policy makers look to fiscal stimulus there will be a blurring of lines between fiscal intervention and monetary actions which casts doubt on the traditional roles of governments and central banks. Landmark fiscal expansions such as the infrastructure projects espoused by President Trump face three key challenges: the identification of projects, the planning lead time to their implementation and their financing. The first two challenges are a matter of timing – will realisation of these projects be sufficiently swift to avoid disappointing the asset markets which have largely priced in the positive economic impacts. On the last matter, in a world of highly indebted governments such spending programs seem unlikely to be financed by the issuance of traditional government debt without serious increase in market yields. Likewise, private capital involvement will not sufficiently bridge the gap, and nor will a change in taxation policies.

We foresee a potential path whereby a new QE program morphs to finance these projects – money financed fiscal policy, or colloquially known as ‘Helicopter Money’. Whilst not our central scenario, we would not be surprised if it was announced that the fiscal projects were financed by newly issued ‘infrastructure bonds’, which qualify for the central bank’s purchase and reinvestment programs, and perhaps pension funds and other institutional investors will be compelled by regulation to hold a portion of their bond allocation in such instruments. Our expectation is for sustainably higher inflation pressures, and as such are looking at protection in our client portfolios against this strategy. We hold a healthy allocation to companies who can exert pricing power over their consumer to protect their profit margins, and are revisiting the case for Gold in portfolios.

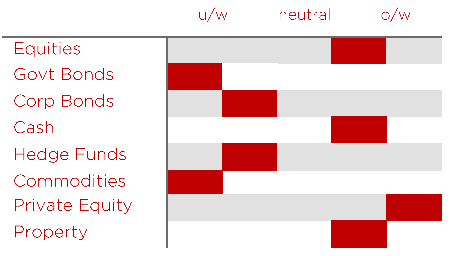

Our latest view on asset allocation positioning

Insights from some of our managers

A credit manager we met recently made a compelling case for global credit selection strategies which look at arbitrage opportunities within capital structures and across market sectors with no regard for geographies. Their thesis is that fixed income is a fragmented market, where most investors only look at Sterling, US, European and Emerging Markets independently – but in comparing global sectors (such as steel) there are value opportunities in picking between US, Indian and Brazilian steel manufacturers which operate in direct competition – regardless of their corporate headquarters’ domicile.

Other news

The composition of the Federal Reserve’s Open Market Committee is likely to change dramatically over the next 15 months, with President Trump able to influence 5 new appointees (out of a total of 12 committee members), including Janet Yellen’s position, whose term ends in early 2018. With the normal ‘rotation’ of voting members, in 18 months’ time there could be as few as 4 FOMC voting veterans in place. Personnel change of such magnitude is likely to herald a change in policy direction – a fact we are very focused upon.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.