How markets have performed (to 16th June 2017)

Equities and bonds came into June with strong momentum – most financial assets (except broad commodities) have delivered positive returns in GBP terms this year. However, the first half of the month saw volatile equities and rising sovereign bond prices. The most significant market event in June was the Fed’s mid-year meeting. A rate hike was fully expected, however parts of their statement were more hawkish than a quarter ago (March).

What we are thinking

When the election was announced in late April, PM May was secure in her position and many were questioning the future of the Labour leader. Now the roles have been reversed, a week is a long time in politics they say and 8 weeks has proved to be a lifetime.

A fortnight on from the unexpected and inconclusive election result the UK is entering the Brexit negotiations this week with no settled government. We expect the stability of the current arrangement, and the leadership mandate of PM May, to be tested over the summer months.

We believe the events of the last few weeks have broadened the range of potential outcomes, but not changed our central view – and therefore we have not changed our investment strategy.

Until the government has been formally appointed, and the Queen’s Speech passed through parliament, there remains a risk that the proposed structure will fail and therefore a (low probability) scenario whereby Labour is given the opportunity to form a government.

As we believed pre-elections, the course of the Brexit negotiations will inevitably be tumultuous and it is likely that UK assets (and most notably the currency) will take their lead from the ebb-and-flow of the negotiations. We hadn’t anticipated, however, the UK entering the negotiations on a weakened stance and we therefore hold a somewhat higher conviction in our bearish outlook for sterling – other than a surprise decision by the MPC it’s difficult to see what good news can drive it significantly higher from here.

In client portfolios, we have refrained from rebalancing equity positions generated through recent capital appreciation, but would be cautious on adding new capital to equities at current levels. Within fixed income our strategy remains to be short duration and only selectively exposed to credit markets. We view elevated cash holdings, and an allocation to gold (for clients where this is appropriate), as insurance against adverse market moves.

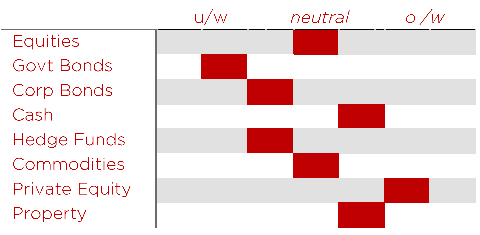

Our latest view on asset allocation positioning

Insights from some of our managers

A private equity investor we met recently stated that it is nearly impossible to ‘buy cheap’ in the current environment, and that returns are being generated almost exclusively by operational and management improvements in the companies. We believe this is a slight exaggeration but agree with the broad sentiment of their statement, particularly when it comes to large deals. Looking for small to mid-market funds has been a core pillar our private equity selection process over the last few years. To highlight the exuberance for private equity in the current market, an Asian venture capital fund managed by Japan’s Softbank has received commitments of $93bn in their first fund close – they are targeting $100bn!

Other news

Earlier this week the MSCI Index announced the inclusion of China’s onshore A-Share market within its Emerging Markets Index. At first, the companies included will be few in number (222 companies), and represent less than 1% of the index. At full weight, which is likely to take years to be implemented, A-Shares could represent 10% of the index.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.