How markets have performed (to end December 2016)

Financial markets continued their upward trend in December, with most asset classes rounding off the year with further gains. Equity markets (developed and emerging) delivered positive gains and fixed income markets reversed the negative performance trend of the previous months. Commodities in aggregate performed well, however precious and industrial metals disappointed on the month.

What we are thinking

In our last newsletter we discussed what we believe is at the root of electorate discontent in the developed economies – ‘unfilled expectations’, and how this is fueling a change in the political landscape. We believe that future historians will look back at the 2000’s as the boundary of an ‘age’, which started in 1789 with the French Revolution. We suggest 19th and 20th centuries should be termed the ‘Democratic Age’ – as democracy grew to be the predominant form of global government. But since the fall of the Berlin Wall the political battle has been changing from left and right to populism and establishment; in most countries there is only one populist party, either “leftist” or “rightist”, but not both. Electorates have learnt that leaders will give them whatever they request, and current leaders seem unable to change that perception – political leaders have become followers of public opinion. The truth is that populism is winning, even when losing due to the influence of mainstream political party policy to attempt to retain power.

Against this backdrop we predict an increase in economic and financial market volatility as a result of political interventions – and a stalling of economic reform in the face of weak mandates and the threat of populist opposition. We made no changes to our high level investment strategy over the month, however within our equity portfolios we reduced exposures to growth equity strategies and funded investments in Small Cap and Value managers. These changes reflect our view that fiscal policy will boost economic activity in the short term, with Small Cap companies and cyclical sectors standing to benefit the most.

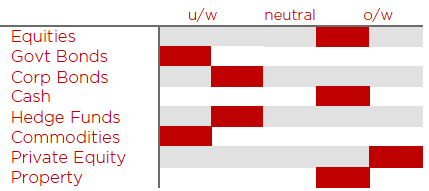

Our latest view on asset allocation positioning

Insights from some of our managers

Equity strategies focused on the “quality” theme, especially those with high consumer staples allocations faced a chastening end to 2016 as investors rushed towards cyclical sectors, and US Dollar earnings exposure in the wake of Trump’s election victory. One of the focused managers in this sector we know well believes the sharp de-rating of this sector provides investors with an attractive valuation point to increase defensive equity positions – with P/E levels now close to a 10-year low and the compounding power of their earnings unaffected.

Other news

The remarkable run of the stock market closing at all-time highs on a near daily basis has led to a collapse of the VIX, a measure of volatility and often an indicator of investor confidence. It can also indicate complacency, as suggested by the fact that the S&P has traded more consistently closer to its 52 week highs in the past four years than ever before. In other words, there has been a near collapse in drawdowns – investors have forgotten what a bad day in the stock market feels like! We might need to brace ourselves for some volatility if any unexpectedly poor economic, political or corporate news is released, particularly with valuations at fair to expensive levels.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.