How markets have performed (to end July 2017)

Late June saw a correlated move downwards in the price of most assets as investors took fright at the raft of hawkish comments from Central Bank officials globally. July saw calm return to the markets and volatility fall close to record lows again. Equity markets recovered well, with Emerging Markets leading the pack (as they have done YTD), whilst yields stabilised and provided support for bonds. Oil performed strongly towards the end of the month, but remains a laggard for the year as a whole.

What we are thinking

We believed that 2017 would mark a turning point, with our expectation being for a boost to global growth and the seeds being sown for a sustainably higher inflation environment, albeit with longer term problems in store for the global economy as the pressures of accumulated debt, disappointing productivity and innovation developments and demographics/populism weigh on future growth prospects.

The first quarter of the year saw this view become the consensus outlook and, combined with high expectations for the Trump administration’s agenda, it drove global markets sharply higher. The second quarter brought disappointments for those investor expectations as the realities of government legislative procedures and some weaker than expected economic data deflated markets.

We retain conviction however that the underlying trend remains and maintain our cautiously optimistic outlook for the medium term. We expect the remainder of 2017 to maintain the synchronized global economic growth cycle, with China’s growth moderation a factor to monitor. Corporate earnings have been strong, supporting the equity markets and likely to lead to continued, but modest, appreciation. We believe that the subdued inflation figures posted so far in 2017 are likely to rise, and with this a risk that bond yields rise as well. We see signs of wage pressures building, notably in the US. Commodity markets seem to be stabilising, removing a key deflationary factor from the recent data. Finally, monetary and fiscal policies remain very accommodative with many austerity measures imposed over the last few years being moderated or repealed. We expect a combination of these factors to contribute to inflationary pressures from here, and believe that policy makers will tolerate elevated inflation numbers since this would have the advantageous outcome of eroding the value of their accumulated debts.

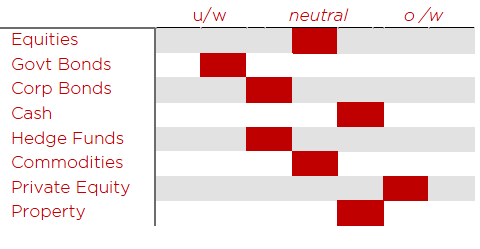

We retain full exposure to equity markets and a cautious view on most fixed income investment classes. For clients with the ability to invest in illiquid strategies (Private Equity and Property) we believe that there are interesting opportunities to pursue in the current market. The recent rise in sterling takes the currency close to the upper end of our expectations, and should this strength persist we are likely to take the opportunity to reduce our exposure in favour of the US Dollar

Insights from some of our managers

One of our Global Value equity mangers succinctly described his investment style as ‘backing the incumbent companies over the new disruptor in an industry’. He gave the example of Tesla’s market capitalization now exceeding that of Ford, the former company sold 76,000 cars in 2016 and the latter 6.6m. He makes the case that unloved incumbent companies often trade at such low multiples that investors can make good returns by believing the incumbent will survive, whereas the disruptor must deliver on its promise to satisfy lofty investor expectations.

Other news

The S&P Information Technology sector (in price terms) set a record high during the quarter, rising above the peak value posted 17 years earlier in March 2000.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.