How markets have performed (to end September 2019)

The third quarter as a whole was positive for most assets, however a series of economic, political and geopolitical factors sparked short bursts of volatility. Global equities started the quarter strongly but pared their gains in August before rallying to the end of September. Japan was the strongest performing market, ahead of the US, with European, Asian and Emerging Markets failing to make significant headway over the summer.

Within equities we witnessed a sharp and rapid style rotation in mid-September as Value style investments recovered all of the prior two months of underperformance against Growth style investments. Bond markets continued their strong returns with government bond yields moving significantly lower over the quarter and re-testing the lows seen over the past decade. Credit remains well supported and to date the corporate defaults (e.g. Thomas Cook) are being treated as idiosyncratic events, rather than a sign of broader sector and market fragility. Gold has continued its upward trend, reaching multi-year highs during the summer months.

What we are thinking

Financial markets this year have presented investors with the unusual situation of equities, bonds, commodities and defensive assets, such as gold, delivering strongly positive returns.

We have discussed in previous notes the belief that equity and bond markets seem to be pricing in different expectations of what is to come. Many of the risk factors which have preoccupied investors for the last 12 months, and beyond, have generally worsened in 2019 – yet the anticipation of looser Fed monetary policy has kept investor sentiment buoyant. Of the risk factors that we have been following closely – recession fears, US-China trade war, Brexit, Chinese economic slowdown, Italian politics and corporate earnings – only one of these risks has significantly abated (Italy), whereas we believe that on balance all other factors are the same or have deteriorated. The US-Chinese trade war has intensified, not diffused as many had expected. The market consensus is that President Trump will seek a resolution as he moves towards his re-election campaign – but this is far from certain, and would require the Chinese to be equally motivated for a deal. However, China’s ‘time-horizon’ for the negotiations stretches beyond November 2020.

The latest releases of economic data have been almost uniformly weaker – with the manufacturing sector in most economies approaching, or in, contractionary territory. Corporate earnings have been downgraded from the optimistic expectations set at the turn of the year and investors will look with great interest at the upcoming earnings releases to gauge the health of the corporate sector.

Given the economic, political and corporate news flow we find it surprising that the market returns have not shown more dispersion. The explosions at the Saudi oil production facility in mid-September barely registered in market behaviour. Neither did the announcement of impeachment moves against President Trump. The belief amongst investors in the ‘Powell-Put’ remains entrenched and after a batch of weaker US economic data in early October all eyes will turn to the next actions of the Federal Reserve.

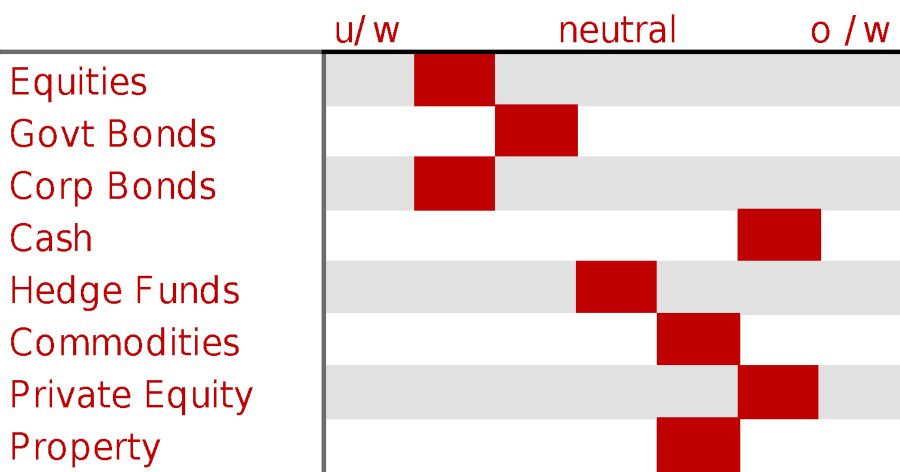

Against this backdrop, we have made few changes to our investment strategy. An underweight position in equity markets has been paired with similar caution in bond allocations (lower interest rate duration risk and higher quality credit focus) and a reasonable allocation to Gold. Given the counteracting forces in the market, we believe that the tension between asset class performance is increasing and consensus may shift more decisively. We retain our conservative positioning, believing that the risks outweigh the opportunities in the current market.

Insights from some of our managers

We attended a thought provoking presentation from a manager that is integrating scientific climate change research into their investment process, specifically looking at expected changes in temperature and weather by locality to influence their investment research. As an example, they talked about the US municipal bond market which typically has long term debt liabilities issues. Recent weather patterns shows that there is an increased incidence of extreme weather events, yet some of the most susceptible municipalities (e.g Gulf Coast and Florida) borrow at the same rates as Northern state municipalities despite the expectation of higher disruption due to weather events and the need to invest in infrastructure to deal with increasing temperatures.

Other news

WeWork bonds have reached new lows as early investors and investment banks are worried that the company will run out of cash next month. Not so long ago the planned IPO was going to value the company at $40-70bn, but in a very short space of time its fortunes have reversed and it is now on the verge of bankruptcy. We are not surprised, given that it is expected to generate an operational loss of $3bn this year. It may still be saved as its biggest backer, Softbank, is rumoured to be stepping in with a debt and equity infusion, potentially giving it full control of the company. But at what cost to its investors?

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.

IMPORTANT NOTICE:

Investors should be aware that with investing capital is at risk, past performance is not necessarily a guide to the future and that the price of shares and other investments, and the income derived from them, may fall as well as rise and the amount realized may be less than the original sum invested. Wren Investment Office limited is authorised and regulated by the Financial Conduct Authority.