How markets have performed (to end June 2019)

The second quarter continued the upward trend of markets set by the exceptionally strong start to 2019, albeit interspersed with some weakness in May. Equity markets led financial markets higher, however a notable feature of 2019 is that most asset classes have delivered a positive return for the year to date. According to Deutsche Bank research, all assets of a panel of 38 that they track (Bonds, Equities, Commodities) showed a positive return in June, only the second time this has occurred since they began the exercise in 2007. The other month that this phenomenon occurred was in January of this year. The conundrum for investors in this scenario is that both risk assets and defensive, ‘safe haven’ assets are rising in tandem. It is very difficult to see an environment where both can be right for a sustained period.

Global equities rose by 6.4% during the quarter, with the US and European markets level-pegging over the period. As trade tension rhetoric heightened, the Asian, Emerging Market and Japanese equity markets were held back on a relative basis. After a weak start to the quarter, government bond yields rallied significantly – for example the UK 10 year Gilt saw its yields rally from a high of 1.2% at Easter to 0.83% at the end of the quarter, a level last seen in the summer of 2016.

The strongest rally of the quarter was reserved for Gold, as the price rallied 11.5% (in Sterling terms) to the highest level seen since 2013. Oil was marginally weaker over the quarter, however in response to increased tensions in the Middle East the price rallied strongly in the latter half of June.

What we are thinking

We wrote in our last note that we expected “a period of market volatility with meaningful rallies and corrections (by which we mean +/-10%) but, overall, markets treading water in absolute terms.” Following the rally of June, equity markets are approaching the highs achieved in 2018 for most markets. However, given the nature of the rally, characterised by a relatively narrow group of growth-oriented sectors and stocks, it doesn’t feel like a “bull” market for all equity investors.

We believe that the markets are currently displaying a high level of nervousness, witnessed by price moves responding to the latest news release, press conference comments or tweet.

It is clear that President Trump, in the run-up to his re-election campaign, is looking to place the blame for any US economic woes that may occur at the door of the Federal Reserve, and in particular Chairman Powell. We are of the view that the unpredictable nature of the current US administration’s approach to diplomacy, geopolitical risks and global trade talks make heightened volatility almost a certainty.

Over the past 6 months there has been a remarkable change in the markets’ expectations for the path of US interest rates. As recently as December of last year the overwhelming expectation (greater than 85% probability) was for at least one more rate hike and many expecting two. Today the expectations have reversed suggesting two rate cuts (for a total of 0.5%) in 2019, and as many as four interest rate cuts by this time next year. This change in sentiment has been against a backdrop of political pressure and softening economic and corporate earnings data.

The equity markets – at their elevated levels – have responded to this policy accommodation and appear to be pricing in the extension of the growth cycle for a little while longer. This scenario could be akin to what we saw in 1998, which presaged a further rally in equity prices to bubble territory in 1999/00.

Viewing the world through the lens of the bond and gold market one might take a more measured appraisal of the outlook, with rallying yields and bullion prices traditionally a signal of investors seeking safe-haven asset exposure.

What the market perception will be of any Federal Reserve policy moves is critical for financial markets. The Fed will be at pains to paint any cuts to interest rates as a preventative measure to support a softer economic environment. Having changed tack on policy announcements a couple of times in his tenure, does Chair Powell have the credibility to uphold confidence? We foresee a potential risk that markets question whether the “Fed knows something more” to justify the scale and pace of easing and investors look for darker clouds on the horizon. If the market expectations of rate cuts are correct, history suggests that this scale of monetary easing is rarely ‘nothing to worry about’ in economic terms.

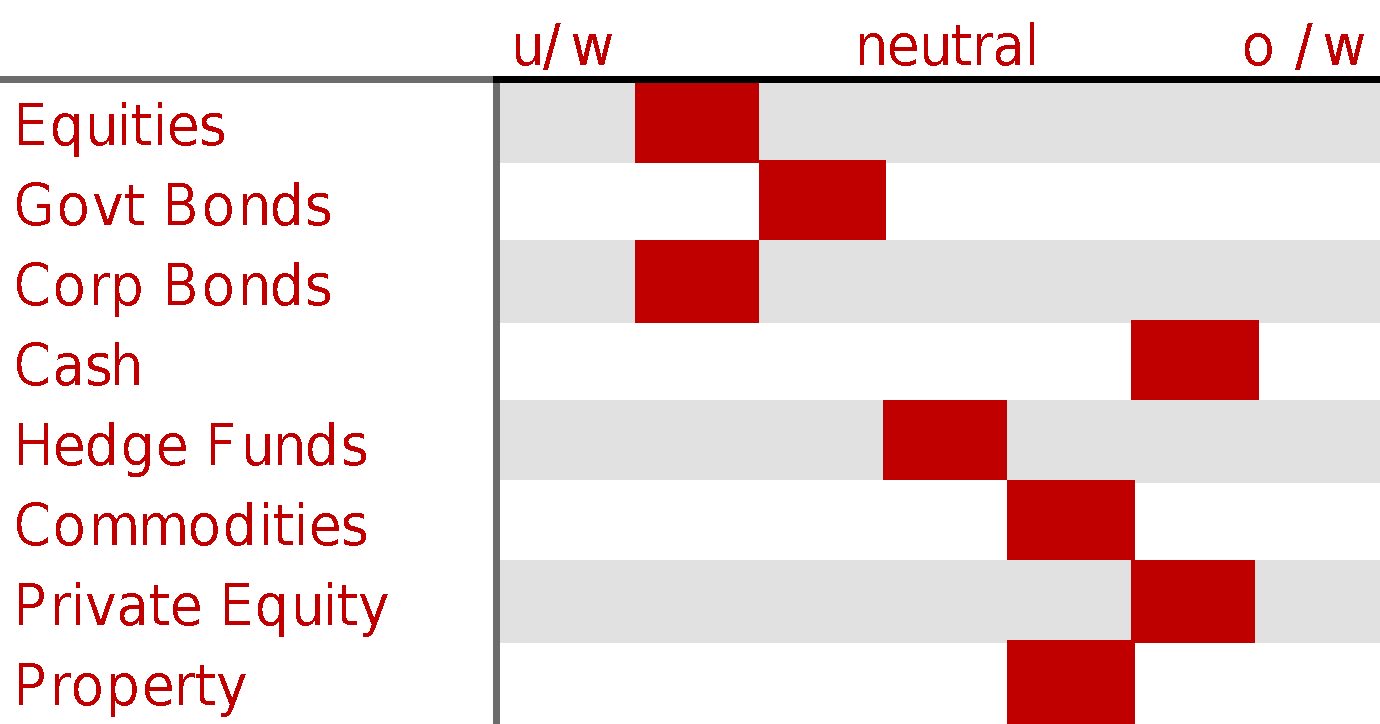

We therefore remain defensively positioned, holding an underweight position in equities and higher risk corporate credit balanced with higher exposure to cash, shorter dated government debt and gold bullion.

Insights from some of our managers

The announcement by Facebook that it intends to launch its own ‘currency’, Libra, has sparked much interest and debate in financial markets. We discussed its potential impact (and disruption) on Western Union, the money transfer service, with one of our managers. Their view is that it’s a potentially exciting innovation, but with several barriers to overcome before it becomes a credible threat. Will consumers trust Facebook, both with maintaining the value of their Libra coin, as well as the privacy element of recording all their transactions and transfers? Some countries, such as India, currently restrict the use of crypto-currencies, so regulatory barriers would need to be overcome for it to become a global competitor to Western Union’s vast network of local agents (over 500,000 locations in 200+ countries).

Other news

This week 10 year German Bund bond yields traded below the ECB policy rate for the first time in history, with all German bond yields in negative territory out until the 2040 maturity bond – this accounts for 90% of the total outstanding value of German debt. In the EU, 9 countries are now recording negative yields for 10 year debt. When tallied together the global bond markets have a total of $13.4 trillion of debt trading at negative yields.

IMPORTANT NOTICE:

Investors should be aware that with investing capital is at risk, past performance is not necessarily a guide to the future and that the price of shares and other investments, and the income derived from them, may fall as well as rise and the amount realized may be less than the original sum invested. Wren Investment Office limited is authorised and regulated by the Financial Conduct Authority.