Update from Wren on COVID-19

We hope that you and your families are remaining safe and healthy during these uncertain times and adapting to working from home.

Like many firms during these last few difficult weeks, we have all been successfully working remotely from home, with full access to our systems and reporting capabilities. Meetings have been conducted virtually and we have been able to continue to advise our clients through the current crisis. From all of us at Wren, we wish you, your families and colleagues well.

How markets have performed (to end March 2020)

Under the shadow and influence of a global health pandemic, historic precedents and financial market records were rewritten at an alarming pace. January and early February started strongly with the optimism and momentum of the exceptionally strong markets of 2019 carrying into the New Year. From the peak of the markets in mid-Feb, investors saw equity markets fall by over a quarter in a matter of weeks. The daily volatility of asset prices and the seizing up of credit markets took investors back to an environment last witnessed in late 2008. Central banks and policy makers slashed interest rates and injected vast amounts of liquidity to quell the panic in financial markets.

Corporate bonds of all credit quality saw their prices fall sharply in March through a combination of increased fears over the creditworthiness of borrowers and a sharp decrease in market liquidity as nervous investors withdrew from the sector. Gold and government bonds proved resilient over the quarter as a whole, however in the midst of the market falls in mid-March all assets, including safe-haven assets, sold off in unison with US Dollar cash emerging as the asset most in demand.

The sharpest falls were reserved, however, for the energy market as Oil suffered twofold; from a sharp decline in demand as a result of widespread economic shut-down across the globe and the announcement by Saudi and Russian officials in early March that OPEC members would break with the prevailing quota agreements.

What we are thinking

We believed the global economy was already showing signs of weakness at the turn of the year and now it seems likely that the pandemic has tipped the world into a recession.

We remain concerned about the impact of a significant economic slowdown on corporate earnings and fear that the current mini rally may be blunted as the second quarter reveals the extent of lost output due to the COVID-19 pandemic. Indeed, it is not unusual to have significant market rallies in the midst of a wider market correction – in the bear market that followed the 2000 technology bubble there were three market rallies of more than 10% and a further three market rallies of more than 20%. A similar trend was observed in 2007-9.

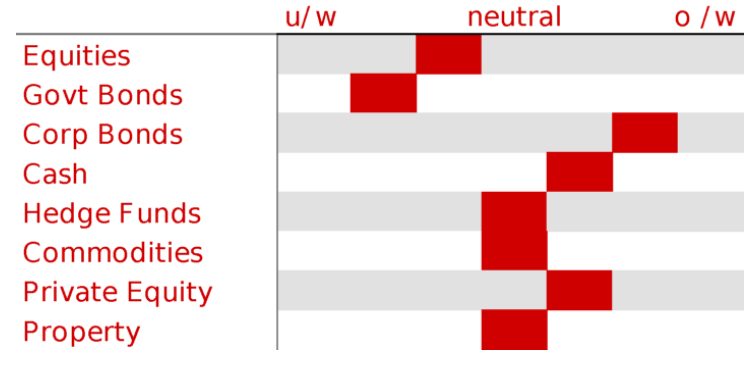

Our investment committee has decided to retain a modestly defensive strategy. We took the opportunity to put some capital to work in portfolios in the depths of the equity market declines but remain slightly underweight.

We have spent considerable time considering the levels at which we believe the equity markets would offer good long-term value, at which point we would look to increase exposure towards strategic weights, and potentially move to an overweight position.

We believe that the moves in the corporate credit markets have been more extreme. Our research suggests that the yields on offer in investment grade and high yield present investors with a margin of safety which exceeds the credit losses experienced historically. We will be allocating capital to this asset class in the coming weeks.

Insights from some of our managers

We have had conversations with numerous private equity managers over the past few weeks and have learned that the first quarter valuations are only expected to capture a fraction of the impact of the COVID crisis. Private equity investors should therefore be braced for a lagged impact, with valuations likely to be marked down further over the coming quarter or two.

Other news

Ruffer Investment Company has received plenty of news coverage, rightly, for its positive performance in March thanks to the derivatives it owned to benefit from a rise in volatility. Another investor, CALPERS (California Public Employees’ Retirement System) was in the news for the wrong reasons. According to press reports, the pension fund invested in tail risk hedging strategies in 2017 but sold them at the end of 2019 because they viewed the ongoing costs of the hedges to be too expensive. Had they held on until March, they would have netted a gain on the hedges of $1bn.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.