How markets have performed (to end March 2019)

The first quarter of 2019 saw a reversal in fortunes for financial markets, a stark contrast to the market falls and volatility which had characterised the final quarter of 2018. The seeds of the market rally were sown on Boxing Day when the US equity market delivered one of its strongest one day rallies in a decade – and this sentiment persisted for much of the first quarter. Unlike 2018, most assets have delivered positive returns for the year to date, with both equity and bond assets providing good returns to investors. Global equities have led the way, with most indices posting a rise of c.10%. Regionally, the US has marginally outperformed other markets, with Japan and Emerging Markets (ex-Asia) lagging. Fixed income returns have been driven by a fall in government bonds yields which has seen the US 10 year Treasury yield move to 2.4% at the end of the quarter from 2.7% at the beginning of 2019. UK 10 year Gilt yields are now at 1%, falling from 1.3% at the turn of the year. Corporate credit spreads have tightened and these assets have outperformed their government bond counterparts. In the commodity sector, oil has rallied significantly (+32% for WTI Crude – in USD).

What we are thinking

In December we thought the scale of market falls had been exaggerated as investor pessimism accelerated ahead of the marginal deterioration in the global economy. As such, we believed there was a good probability of a market bounce in 2019, although we expected that this would be capped by a less supportive economic outlook.

The market rally so far this year has been stoked by the conciliatory actions and words of the US Fed during the first quarter, as investor expectations of further rate hikes were significantly diminished (a growing proportion believe the next move may be a rate cut). As we stand today, we believe that the equity and bond market performances for 2019 are signalling contradictory views. The equity market is seemingly expecting a re-acceleration of the cycle and government bond markets are pricing in a more difficult outlook.

The conclusion of our House View work for 2019 outlined a scenario where the Fed acts in a ‘hesitant’ manner, rowing back from conducting a succession of further rate hikes (as indicated by Chair Powell in mid 2018). In this environment we expect to see a period of market volatility with meaningful rallies and corrections (by which we mean +/-10%) but, overall, markets treading water in absolute terms. Looking at historical precedents, we think that this scenario could echo 1999/2000 and 2006/07. We believe that a likely source of market volatility in 2019 will be the inactivity of the Fed in response to changes in the underlying economic data, making its policy seem accommodative/restrictive in turn to an investment community which has become accustomed to Central Bank intervention on a frequent basis over the last decade.

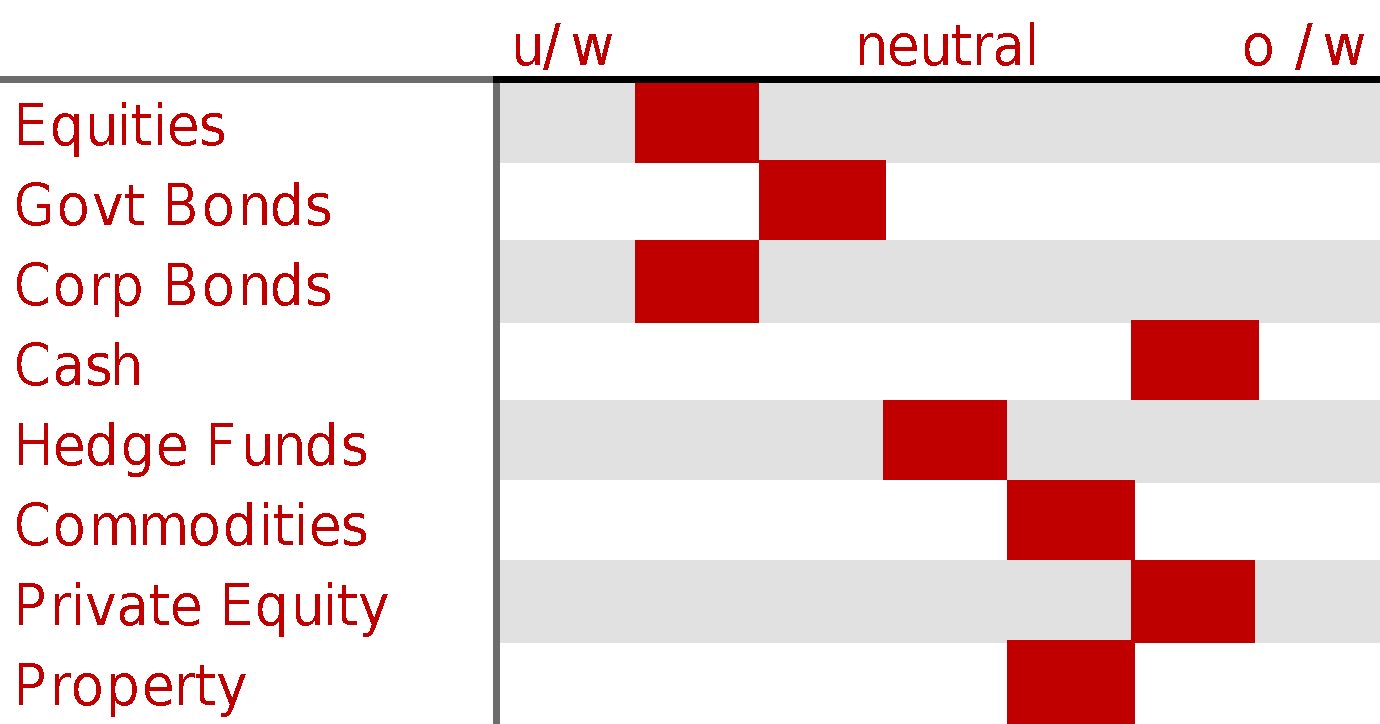

Our broad strategy is aligned with the cautious outlook priced into the bond markets – we retain a defensive stance in anticipation of more difficult times ahead.

During the first quarter we took the opportunity provided by the very strong equity market rallies to reduce risk exposure even further. We retain our short duration and cautious credit positioning within fixed income.

For sterling portfolios we took the opportunity to increase sterling currency exposure. There remains significant uncertainty regarding the progress and path of the Brexit negotiations, however we believe that the market offered us an opportunity to position portfolios for a more positive outcome than had been priced in at below 1.30 against the US dollar.

Insights from some of our managers

The volatility of individual stock prices in Asia, and the rapid recovery in 2019 to date was highlighted to us in a recent manager meeting. The manager, a value style investor, was active during the difficult markets of the fourth quarter buying into Chinese consumer facing companies which they believed were unjustifiably de-rated on concerns of the ongoing US-China trade dispute. A quarter later many of these companies are on the way out of the portfolio, having posted price rallies of 40-50%, on average, and in one case close to a 70% rally from its lows in October

Other news

2019 is expected to be the year of the “Unicorn” tech IPO – with Uber, Pinterest, Airbnb, Palantir and Slack all expected to list. Lyft had its IPO last week, valuing the company at $24bn. It made losses of $911m last year. Uber has narrowed its losses to $3.3bn last year from $4.5bn in 2017 and is expected to reach a valuation of $100bn or more. The question for investors is whether these valuations are justified given the time it will take for future profits to emerge, if at all. Twitter took 16 quarters to make a profit post IPO, Amazon took 18 quarters, yet Facebook only took 2 quarters. Snap and Dropbox are yet to make profits.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.