How markets have performed (to November 2017)

Equities performed strongly across the board in absolute terms. Japan was a clear front-runner relative to other markets. A snap election resulted in a continued strong mandate for PM Abe, and markets reacted positively to the news. The S&P 500, in USD terms, has now delivered a positive return for the last 12 months in succession – which according to a Deutsche Bank report equals a record set in 1949-50 and 1935-36. European assets held firm despite the continued uncertainty and unrest in Spain. Fixed income markets displayed a little more volatility, but for no significant movement in performance during the month. In commodity markets, agricultural commodities were a little weaker, but energy and oil rose strongly, with crude hitting a new high for the year on fears of a supply cut. Gold fell during the month as investor worries eased and demand for the safe haven asset reduced.

What we are thinking

We see the current market environment as having a finely balanced range of economic and corporate

outcomes offset by a higher than usual set of risks and uncertainties. In aggregate we believe the positive

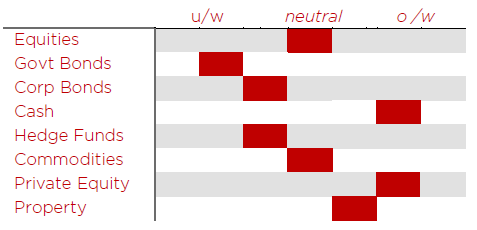

forces outweigh the risks in the near term and our investment strategy keeps us overweight risk assets.

The case for the positive is well defined: synchronized global growth, strong corporate earnings results and

continued accommodative policy from central banks globally. We worry about: the lack of visibility in the

global economic cycle, inflation (as we have mentioned previously), geopolitics, the difficulty central banks will

encounter in removing their accommodative policy measures and what we believe are signs of complacency

and pro-risk behaviour by market participants. These include: volatility at multi year lows, some stocks

(“FAANG”) are considered infallible, ETFs are receiving huge inflows, junk companies and countries are issuing

long bonds, and the extraordinary rally in bitcoin.

All assets are highly valued, and expected returns for all asset classes are low by historical standards. Our

investment strategy follows three themes:

- Be prepared to accept lower returns than in the past

- Take lower risk than usual

- Try to change market risk to manager risk. We favour illiquid assets in which manager risk dominates

In summary, we retain our positive outlook for risk assets We are selective in our allocations to corporate credit,

wary of interest rate duration exposure and see value in the capital preservation and defensive qualities of cash

and gold within a multi-asset portfolio.

Insights from some of our managers

One of our European equity value managers put forward a compelling case for shipping stocks, specifically oil and refined oil product tankers. He observes that the scrappage of these tankers is running well ahead of new capacity building, and that many of the most highly levered operators have gone to the wall in the face of a difficult operating environment. Taking a medium term view, the manager believes the fleet capacity supply/demand balance will shift in favour of the surviving tanker operators; day rates are 25% of historic average at the moment. The current market prices imply that this difficult environment will persist. However, we tend to agree with our manager that the demand for oil transportation is not disappearing in the near term and an interesting opportunity exists for patient value investors willing to take an early stance that the cycle for these stocks is turning.

Other news

The latest Investors Intelligence survey of US investor sentiment recorded the highest ratio of Bulls to Bears since 1987. Such sentiment data has no direct links to subsequent market performance – but is another indicator of the prorisk behavior we believe is prevalent in investment markets, and one of the key risks in the current environment.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multifamily offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.