How markets have performed (to end November 2017)

Financial assets have delivered strong returns across the board in 2017, led by equity markets and some segments of the commodity universe (energy and some industrial metals). Fixed income markets have been more muted as investors balanced the need for yield with the prospects of inflationary pressures and central bank rate rises. On the month there was some volatility in the markets, especially the US, as the progress of the tax reform bill was mirrored closely by financial markets. Gold has not delivered significant returns to investors in the year as a whole, but performed well in the few periods of modest market stress that have occurred.

What we are thinking

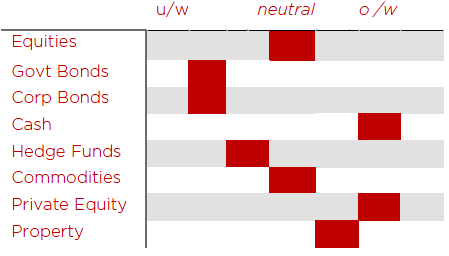

During the month we held our annual investment House View meeting to review, discuss and formulate our medium term investment strategy. Our starting point was the strategy applied in 2017, which called for a pro-risk positioning of an overweight allocation to equities, illiquid assets and credit (selectively), at the expense of government debt and interest rate duration, which we perceived to be at risk of a sell-off.

Geographically and sector wise, our clients’ portfolios have been underweight the US market in favour of Asia and European equities, growth equity allocations have been reduced in favour of value style managers and we have sought greater exposure to small cap equities in anticipation of stronger economic growth.

It is said that bull markets do not die of old age, but are typically killed off by monetary tightening cycles. We have looked to history in order to draw parallels and potential lessons to inform our medium term investment views; focusing specifically on the late 1930s, the late 1960s and the lead up to the 2008 crisis.

For now we remain fully weighted in equities, but are reducing our exposure to the corporate high yield sector where we see the greatest divergence of value and risk. After a largely one-way flow of assets to these bonds, for the best part of a decade, any reversal might expose a less liquid market and lead to larger than expected volatility. We are also starting a project to explore whether commodity markets offer an attractive investment opportunity, following several years of volatility and some torrid performance.

Insights from some of our managers

We were reminded in a recent meeting of an increasingly common practice amongst some secondary private equity funds, called stapled commitments. Secondary funds set out to buy existing commitments from investors who wish to sell their interests, sometimes for portfolio management reasons or as forced sellers if they are not able to fulfil their commitment obligations. Over the last decade this has been a profitable theme, providing liquidity at a discounted price to asset values. However, this has recently become more competitive and, in return for permitting secondary transactions to complete, some private equity managers (general partners, or GPs) compel the secondary investor to commit capital to their new fund-raising capital – a ‘stapled’ investment. We fear this will lead to some unwanted surprises for secondary investors in the coming years as they discover the portfolio they hold is not solely comprised of older vintage fund investments which are returning capital as assets are sold, but also hold new investment pools which are in drawdown mode and won’t be returning capital for as long as a decade.

Other news

All of us at Wren Investment Office would like to send you and your families our very best wishes for Christmas and the New Year. May 2018 bring you happiness, good health and fortune.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.