This article describes our investment beliefs, relating to markets, that constitute the basis upon which strategic and tactical decisions are taken by Wren and its alliance firms, MdF Family Partners and WE Family offices. They are designed to ensure full alignment between the values and responsibilities of our employees and clients, and of the alliance firms.

Market Investment Belief 1: Markets are very efficient over the short term – we don’t try to time markets

Most financial markets are followed by a sufficient number of people so that any piece of news that appears is immediately reflected into prices. This means that being faster than the market to benefit from any news release is a futile adventure with almost no chance of success. This slim opportunity is further reduced by major investment banks and asset managers spending millions building quantitative trading infrastructure to gain millisecond advantages in placing market trades. Furthermore, trading costs are substantial, and when executing continuous trades these costs can rise to a significant level.

As a result, we at Wren Investment Office, WE Family Offices and MdF Family Partners do not believe in taking short term trades based on the latest published information. We do not engage in market timing, by which we mean selling an asset such as equities or bonds and keeping the proceeds in cash with the intention of reinvesting soon at a more advantageous price level. It takes two trades to time a market successfully, and often if one trade looks brilliant, the second will make you feel foolish – and vice versa.

This philosophy applies to the asset allocation of our clients as well as the managers we select to invest with.

Market Investment Belief 2: Greed and Fear create inefficiencies in the financial markets in the medium term

Beyond the very short term (by which we mean months or quarters) markets are made by people and hence tend to be dominated by psychological factors of greed and fear. These forces are extremely strong and they can make all assets deviate substantially from their fair value. This gives active managers an opportunity to add value in the markets in which they operate.

Occasionally our investment research will identify an economic trend or market behaviour which tilt the odds of performance in favour of certain assets or sectors. We will use this information to tilt client portfolios away from the strategic asset allocation to capture the opportunity we perceive. This differs from market timing in two important respects: time frame and degree. Our tilt decisions are typically based on a time horizon of at least 6 months and sometimes years. The sizes of tilts within equities or bonds tend to be relatively large, whereas those between equities and bonds tend to be smaller to reflect the wider range of possible results. We aim to spread the risk of one or more of our tilt decisions being wrong by having a number of tilts in the portfolio and by ensuring they do not all react in the same way to the same events.

Market Investment Belief 3: Financial markets are mean reverting and efficient in the long term

For every asset we believe there is an equilibrium value to which they revert, even if it takes a long period of time to do so. This reversion period will differ across assets, but academic research suggests with high confidence that this process takes a maximum of 18 years. In most cases however, it is substantially much shorter than that and the whole adjustment can occur in just a few months.

We believe that investment processes predicated upon the accurate forecasting of short term asset performances are unlikely to succeed. It is an easier task to assess the current valuation of assets, and as markets return to their fair value over time, the long term returns can be estimated with a certain degree of accuracy, the predictability of returns increases within investment time horizon allowed.

Market Investment Belief 4: Adding value by active management is very difficult but not impossible.

Active management can add value beyond fees and costs if there is an identifiable competitive advantage around which the investment process is built and consistently applied. But even in those cases it is not reasonable to expect outperformance over all time periods as investment styles rarely work in every market condition – good managers occasionally experience episodes of poor performance. We seek to understand these processes and alter portfolio exposures depending on our market views.

For managers to add alpha, they need to take substantial bets relative to their benchmark. As a consequence, the best approach is to diversify across several managers within the same asset class, creating a complementary blend of investment styles which is expected to deliver superior returns over a market cycle.

When we deem an investment market to be efficient and well researched, the opportunity for active managers to add value without taking excessive risks is very much reduced. That can also happen when trading costs are excessive. In these cases, passive indexing is our preferred approach, although we are cognisant that this is guaranteed to underperform by the amount of the passive funds’ total expense ratio. We may also use passive strategies to execute investment views more rapidly.

Market Investment Belief 5: Illiquidity deserves a premium

Liquidity is an advantage, as it allows for an exit of an investment at a known price at any time. The value of illiquidity is often underestimated, and we find many investment ideas that do not fully compensate the client in terms of potential returns relative to the liquidity which they are surrendering.

The illiquidity premium on offer to investors varies over time, and is closely correlated with investor sentiment, risk appetite and the availability of capital. Judicious commitment to illiquid strategies during periods of elevated illiquidity premia has the potential to significantly boost investment returns for those who are in a position to lock up their capital.

Market Investment Belief 6: Investment Time horizon is crucial for evaluating investment decisions

A long time horizon allows investing in illiquid assets (if the reward is proportional to the risk) and accepting volatility of returns. However, time horizons should be carefully evaluated. It is not only the terminal time horizon that counts – there are usually intermediate liquidity needs which need to be satisfied. Furthermore, regular portfolio valuations and performance evaluation need to be taken into account because they risk shortening the perceived time horizon.

Market Investment Belief 7: Risk and return are tied together. Never trust an investment proposition if you can’t see the risk (and how the promoter is being paid!)

Although there are no risk free returns, there are many return free risks. These investments, which imply that the investor is not properly compensated for the risk he or she is asked to take, should always be avoided. A risk free return is a convenient academic assumption that does not occur in reality. A bank deposit is subject to the solvency of the bank and, if small enough, the guarantee of the government behind the deposit system. Government securities retain an inflation risk if a sovereign power decides to reduce it real debt burden by inflating away the value of its liabilities – the assets of savers. Every expected return must have an associated risk. If such a risk is not identified, we would never recommend an investment. Good investment opportunities appear when the risk is identified and understood, and it is estimated that the market has underpriced that risk or that that risk can be reduced.

Market Investment Belief 8: Income is a key component of investment return, its importance increasing with the investment horizon

Strategies where the investor is paid a stable income whilst waiting for capital gains are often the most attractive. This feature of investment return is stable, and provides the investor the choice of where to redeploy the capital. It may be attractive to reinvest the capital in the asset which generated the income, or to reallocate the funds to another asset within the portfolio which offers more attractive prospective returns.

Market Investment Belief 9: A patient and contrarian approach is required to exploit market inefficiencies

Investment opportunities and inefficiencies are best exploited by taking an opposite view to consensus. In the vast majority of circumstances, but not all, this behavioural bias lends itself to valuation based investment strategies. As a result our client portfolios will tend to have a tilt towards value managers, or other styles that are out of favour at that time.

Similarly, a contrarian discipline applied to asset allocation and portfolio management will add value in the long run. The two key disciplines are systematic rebalancing (selling outperforming assets to reinvest in those which have underperformed) and averaging into or out of the market to reduce the potential market timing impact of a single trade.

Market Investment Belief 10: Capital preservation is at the heart of long term wealth accumulation

In the spirit of Buffet’s two rules of investment, avoidance of losses is the foundation of stronger capital appreciation in the long run.

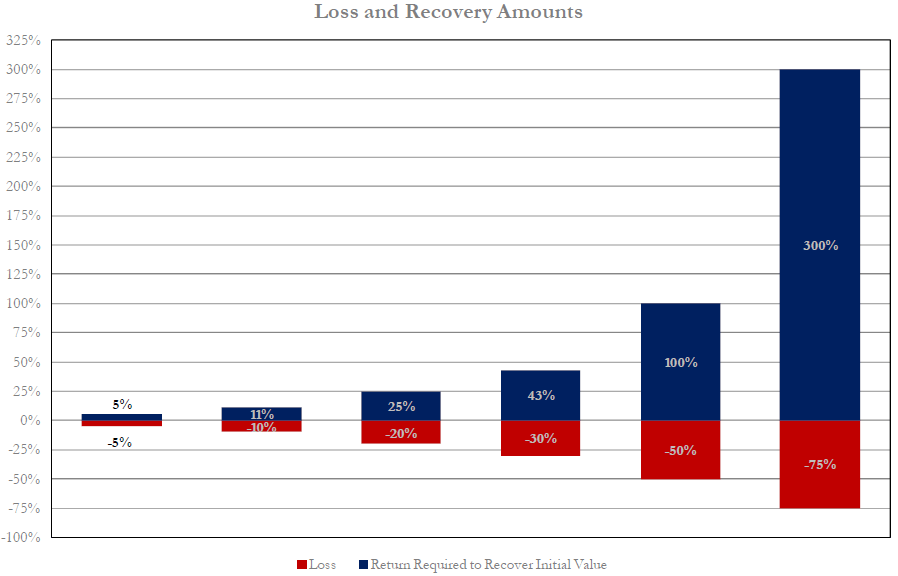

Mathematically, what declines must climb back more to reach break even. If the price of an investment drops 25% it must recover by 33% to return to its starting point. If it falls 50%, then 100% growth is needed to recover the starting value.

That is why it is important to favour managers with the skills to structure their portfolios to fall less when everything else falls and to recover in line with the others. Such managers often display a bias in their processes and selection of investments.

See below a chart that illustrates the commensurate portfolio performance required to compensate for the value lost by the market declines.