How markets have performed (to end September 2017)

Commodities were the best performing asset in the month with oil leading the way as the price ticked above $50/barrel. Equity markets were largely muted, however the German DAX rallied strongly as the election result allayed investors’ fears. Bonds and currencies saw increased volatility. In the UK, the 10yr yield jumped 30bp as markets priced in the possibility of a rate hike, and US yields saw a more gradual rise of a similar magnitude. Sterling against USD hit 1.36 (from below 1.30 at the beginning of the month) before retracing some gains before month end.

What we are thinking

At the centre of our recent Investment Committee discussion was an assessment of the sustainability of the synchronised economic expansion witnessed in the developed and emerging markets. We believe that the current benign conditions will remain for the foreseeable future, and therefore provide a supportive backdrop for risk assets. Our expectation for inflationary pressures to assert themselves in a world of low unemployment, accommodative monetary policies and continued economic expansion has thus far proved incorrect. We believe it remains a case of when, and not if, inflation will return and protecting against this risk remains a key focus of our portfolio construction strategy.

We remain wary of interest rate risk within fixed income portfolios, and have growing fears for the health of the corporate credit market. The last years have seen a wall of capital flow into the bond markets from investors forced to accept greater investment risk to source income. The balance of power shifted towards the borrower, with many companies able to raise significant debt financing at low rates and negotiating loose covenants. In many situations, this debt was used to return capital to the equity holders, increasing the leverage of the balance sheet. We believe these market conditions call for a discerning approach to credit allocations – low interest rates, high leverage and weak covenants are a potentially toxic mix for investors (the lenders). We are especially concerned about the scenario where rising interest rates trigger financial difficulties for companies who’ve assumed too much debt and cannot service or refinance their debt as interest rates rise. The summer saw Toys ‘R’ Us in North America file for bankruptcy under the weight of its debt, we hope this is an isolated incident rather than a “canary in the coal mine”. An area of fixed income we hold in higher standing is emerging market debt, where we believe stronger fundamental data, economic and political reforms in many countries, falling interest rates and low inflation combine to offer a potentially interesting investment opportunity.

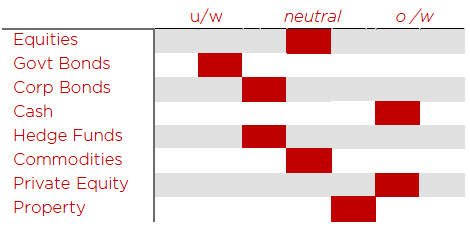

In summary, we retain our positive outlook for risk assets – centered on equity markets and illiquid asset allocation. We are selective in our allocations to corporate credit, wary of interest rate duration exposure and see value in the capital preservation and defensive qualities of cash and gold within a multi-asset portfolio.

Insights from some of our managers

A specialist manager in the consumer space extolled the virtues of focusing on over the counter medical products vs the traditional food, beverage and personal care categories. The argument put forward is that the margins charged are higher, and brand loyalty is superior – when you are ill consumers will typically go for the tried and trusted product and won’t experiment with new treatments or be swayed by special offers. His strategy extends to the emerging markets where this powerful consumer behavior trend is linked with expanding personal incomes.

Other news

A note circulated by RMG Investment drew attention to some of the anomalies of the passive financial markets. A 30yr Russian government bond (USD), a large holding in some Emerging Markets ETFs, is trading at a mere 0.4% yield premium to the US 10yr Treasury. This meagre yield premium, for a bond 20 years longer in maturity and ranked sub-investment grade in credit quality, indicates some irrational capital allocation in the fixed income markets.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.