How markets have performed (to end March 2018)

After an extended period of benign markets, the forces of loose monetary policy, political rhetoric, trade policies, asset valuations and investor sentiment resulted in more uncertainty and market volatility during the first quarter of 2018. Looking to history, it is of course the exceptional lack of volatility in 2017 which stands out as the aberration – financial markets by their nature are volatile and 2018 is a return to normality. Most developed equity markets posted a negative return for the quarter, although the emerging markets outperformed, with many finishing in positive territory for the year to date. Having started 2018 on a weak footing, government bond yields rallied as equity markets stumbled to leave returns broadly flat for most markets at the end of the quarter. Emerging market debt fared better, but credit lagged other fixed income assets. Gold has benefitted from a modest flight to safety in the recent market turbulence.

What we are thinking

The last quarter has seen two significant developments in our view. First, the confirmation of the US tax legislation providing a swathe of tax cuts which has led to optimism over the potential for a new leg of US corporate earnings growth, capital expenditure and investment funded by overseas earnings repatriation and improved domestic earnings. Secondly, the shift of the US administration towards implementing trade tariffs and the concern that this will spark widespread trade disputes, retaliation and protectionism. This second development has the potential to overwhelm the optimism of the first.

Global economic data has remained robust to date, and we expect it to remain so unless trade tensions escalate further from here. With global central banks, led by the US Federal Reserve, looking to remove extraordinary monetary policy measures and raise rates we are wary of the risk that political policy, investor sentiment and monetary actions fall out of synch and combine to form an economic downturn.

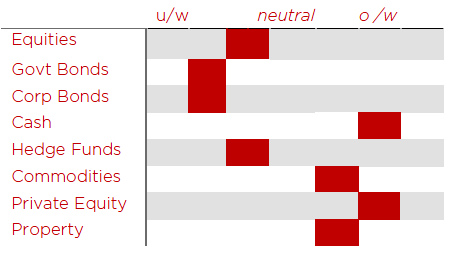

Our investment strategy has changed during the quarter to reflect the first step of our growing concerns on the outlook. Early February was characterised by a bout of market weakness, initially triggered by stronger than expected data in the US causing fears of inflation and further rate hikes. This sell-off was exacerbated by ‘short-volatility’ ETFs which lost significant capital value as market volatility rose. In early March, following a market rebound and what we perceived to be darker clouds gathering, we took a decision to reduce risk further in portfolios by taking equities to a modest underweight position. As discussed in our House View, we believe that a recession is likely within the next 3 years, most probably towards the end of that period. We view the modest underweight position we have taken as the first of a succession of reductions.

Insights from some of our managers

An Asian manager we met presented data on 2017 Asian market returns that showed an almost perfect correlation between market capitalisation and share performance. If a portfolio was not well represented in mega cap growth technology names (Tencent, Alibaba, Baidu etc) it was already at a significant disadvantage. To this end it is impressive how many of our preferred Asian equity managers delivered strong returns through stock selection and diversified portfolios rather than concentrated bets by sector, size and market allocation.

Other news

JP Morgan recently published a fascinating article about Tesla. Its equity market capitalisation per vehicle produced is over $400k (all other car manufacturers are less than $50k), it is consistently disappointing on its production numbers, it is burning through cash at an extraordinary rate and its debt is yielding 300 bps more than that of Ford and GM. Despite all that, four well known brokers have year end stock price targets at 40-50% above its current price.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.